New Tax Regime vs Old Tax Regime: Which is the Best Option for You? (FY 2025-26)

Table of Contents

1. New Tax Regime — What Is It?

2. Old Tax Regime — What Is It?

3. New vs Old Tax Regime — Full Comparison

4. Which Tax Regime Should You Choose?

5. Example Calculation — ₹15 Lakh Income

6. Frequently Asked Questions (FAQ)

7. Conclusion & Recommendation

Every year when income tax filing season arrives, one question dominates every salaried person’s mind — “New Tax Regime vs Old Tax Regime: which one should I pick?” After Budget 2025, this debate has become more critical than ever, because the government made historic changes to the new regime. In this comprehensive guide, we compare both regimes with tax slabs, deductions, real examples, and expert tips — so you can make the smartest financial decision for FY 2025-26.

1. New Tax Regime — What Is It?

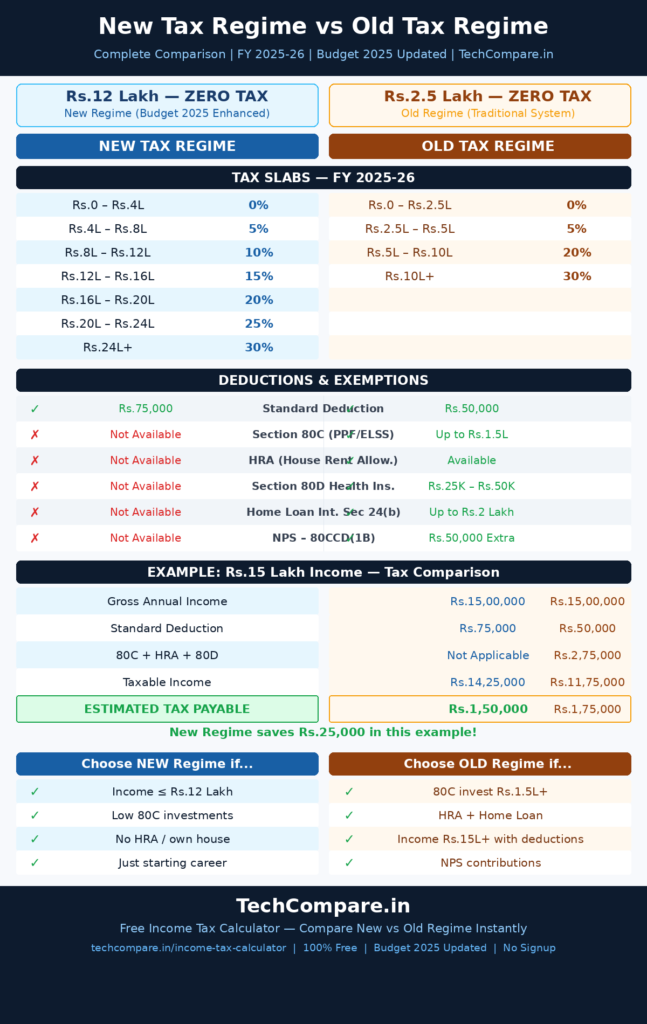

The New Tax Regime was introduced in Budget 2020 and made the default regime from FY 2023-24. Budget 2025 dramatically enhanced it, making income up to ₹12 lakh completely tax-free under the revised Section 87A rebate. For salaried employees with a ₹75,000 standard deduction, this effective zero-tax limit extends to ₹12.75 lakh. The trade-off: most popular deductions and exemptions are unavailable.

New Tax Regime — Tax Slabs FY 2025-26

| Income Range | Tax Rate |

| ₹0 – ₹4 Lakh | 0% (Nil) |

| ₹4 Lakh – ₹8 Lakh | 5% |

| ₹8 Lakh – ₹12 Lakh | 10% |

| ₹12 Lakh – ₹16 Lakh | 15% |

| ₹16 Lakh – ₹20 Lakh | 20% |

| ₹20 Lakh – ₹24 Lakh | 25% |

| Above ₹24 Lakh | 30% |

Important: Income up to ₹12 lakh is completely tax-free under the New Regime due to the enhanced Section 87A rebate announced in Budget 2025. This is a major relief for the middle class.

2. Old Tax Regime — What Is It?

The Old Tax Regime is the traditional system that has been in place for decades. While its tax rates are higher, it allows taxpayers to claim a wide range of deductions and exemptions — including Section 80C investments (up to ₹1.5 lakh), HRA (House Rent Allowance), Section 80D health insurance premium, Home Loan interest under Section 24(b), and NPS contributions. For those who actively invest and plan their taxes, this regime can significantly reduce their tax outgo.

Old Tax Regime — Tax Slabs FY 2025-26

| Income Range | Tax Rate |

| ₹0 – ₹2.5 Lakh | 0% (Nil) |

| ₹2.5 Lakh – ₹5 Lakh | 5% |

| ₹5 Lakh – ₹10 Lakh | 20% |

| Above ₹10 Lakh | 30% |

Note: Under the Old Regime, income up to ₹5 lakh is effectively tax-free due to the Section 87A rebate of ₹12,500.

3. New Tax Regime vs Old Tax Regime — Full Comparison

Here is the most comprehensive side-by-side comparison of the new tax regime vs old tax regime for FY 2025-26:

| Feature | New Tax Regime | Old Tax Regime |

| Tax-Free Income Limit | ₹12 Lakh | ₹2.5 Lakh |

| Standard Deduction | ₹75,000 | ₹50,000 |

| Section 80C (PPF/ELSS/LIC) | Not Available | Up to ₹1.5 Lakh |

| HRA (House Rent Allowance) | Not Available | Available |

| NPS — Section 80CCD(1B) | Not Available | ₹50,000 Extra |

| Health Insurance — Section 80D | Not Available | ₹25,000–₹50,000 |

| Home Loan Interest — Sec 24(b) | Not Available | Up to ₹2 Lakh |

| Home Loan Principal — Sec 80C | Not Available | Included in 80C |

| Leave Travel Allowance (LTA) | Not Available | Available |

| Default Regime (from FY 2024-25) | Yes — Default | No |

| Simplicity | Very Simple | Complex |

| Annual Regime Switch (Salaried) | Allowed | Allowed |

| Annual Regime Switch (Business) | One-time only | Flexible |

4. Which Tax Regime Should You Choose?

The new tax regime vs old tax regime decision depends entirely on your income level and how much you invest. Here is a clear guide:

Choose the New Tax Regime if…

- Your annual income is ₹12 lakh or less

- You do not invest heavily in 80C instruments (PPF, ELSS, LIC)

- You do not receive HRA or live in your own house

- You are a fresher or just starting your career

- You prefer simplicity over tax planning complexity

- Your employer does not offer major allowances

Choose the Old Tax Regime if…

- You invest ₹1.5 lakh or more in PPF, ELSS, or LIC annually (Section 80C)

- You receive HRA and pay significant rent

- You have a Home Loan with interest exceeding ₹2 lakh per year

- You contribute to NPS (additional ₹50,000 deduction under 80CCD(1B))

- Your annual income exceeds ₹15 lakh with high deductions

- You have dependents and pay health insurance premiums (80D)

Pro Tip: Calculate your tax liability under BOTH regimes before deciding. The regime that gives you lower tax is your best choice. Use TechCompare.in’s free Income Tax Calculator to compare in seconds — no signup needed.

5. Example Calculation — ₹15 Lakh Annual Income

Let us take a practical example. Assume your annual salary is ₹15 lakh and you claim the following deductions: Section 80C — ₹1.5 lakh, HRA — ₹1 lakh, Section 80D — ₹25,000.

| Detail | New Tax Regime | Old Tax Regime |

| Gross Income | ₹15,00,000 | ₹15,00,000 |

| Standard Deduction | ₹75,000 | ₹50,000 |

| 80C + HRA + 80D Deductions | Not Applicable | ₹2,75,000 |

| Taxable Income | ₹14,25,000 | ₹11,75,000 |

| Estimated Tax Payable | ₹1,50,000 ✓ LOWER | ₹1,75,000 |

Result: In this example, the New Tax Regime saves ₹25,000 in tax. However, if your deductions are higher (e.g., ₹3.5 lakh+), the Old Regime may save more. Always calculate both before choosing.

6. Frequently Asked Questions (FAQ)

Can I switch between regimes every year?

Yes — salaried employees can switch between the New and Old Tax Regime every year at the time of filing their ITR. However, individuals with business income or self-employed professionals can switch back to the Old Regime only once after opting for the New Regime. The switch must be declared at the beginning of the financial year.

Which deductions are allowed in the New Tax Regime?

The New Tax Regime allows Standard Deduction of ₹75,000, employer contribution to NPS under Section 80CCD(2), Agniveer Corpus Fund deduction, and certain state-specific allowances. Major deductions like 80C, HRA, 80D, and Home Loan interest under Section 24(b) are not available.

What changed in Budget 2025 for New Tax Regime?

Budget 2025 was a game-changer for the New Tax Regime. The Section 87A rebate was increased, making income up to ₹12 lakh completely tax-free (previously ₹7 lakh). New tax slabs were introduced with more gradual rate increases. The Standard Deduction was also raised from ₹50,000 to ₹75,000 for salaried employees and pensioners.

Is the New Tax Regime better than Old Tax Regime in 2025?

For most taxpayers — especially those earning up to ₹15 lakh with limited investments — the New Tax Regime is now the better choice after Budget 2025. However, high earners with substantial deductions (₹3.5 lakh+) may still benefit more from the Old Tax Regime. The key is to run the numbers for your specific situation.

What is the income tax slab for FY 2025-26?

Under the New Tax Regime: 0% up to ₹4L, 5% for ₹4-8L, 10% for ₹8-12L, 15% for ₹12-16L, 20% for ₹16-20L, 25% for ₹20-24L, and 30% above ₹24L. Under the Old Tax Regime: 0% up to ₹2.5L, 5% for ₹2.5-5L, 20% for ₹5-10L, and 30% above ₹10L.

Official Government Resources

For official and verified information, refer to: Income Tax Department — incometax.gov.in | CBDT — cbdt.gov.in

Related Tools on TechCompare.in: Income Tax Calculator | SIP Calculator — Grow Wealth Faster | PPF Calculator — Save Under 80C | EMI Calculator

7. Conclusion & Expert Recommendation

The new tax regime vs old tax regime debate has a clear winner for most taxpayers after Budget 2025 — the New Tax Regime. With ₹12 lakh completely tax-free and simplified slabs, it is the smartest choice for salaried individuals earning up to ₹15 lakh with moderate investments. However, if you are aggressively investing in PPF, ELSS, Home Loans, and NPS — the Old Tax Regime could still save you more money.

The golden rule: never pick a regime based on assumptions. Always calculate your exact tax liability under both regimes, compare, and choose the one that puts more money back in your pocket.